In a word, a reverse home loan is a loan. A property owner who is 62 or older and has significant home equity can obtain versus the worth of their house and get funds as a swelling amount, fixed regular monthly payment or line of credit. Unlike a forward mortgagethe type used to buy a homea reverse mortgage does not need the homeowner to make any loan payments.

Federal regulations need lending institutions to structure the deal so the loan quantity doesn't exceed the house's value and the customer or borrower's estate won't be delegated paying the difference if the loan balance does become larger than the house's worth. One way this might occur is through a drop in the house's market worth; another is if the debtor lives a long time.

On the other hand, these loans can be costly and intricate, along with subject to frauds. This short article will teach you how reverse home mortgages work, and how to protect yourself from the risks, so you can make an educated choice about whether such a loan may be best for you or your moms and dads.

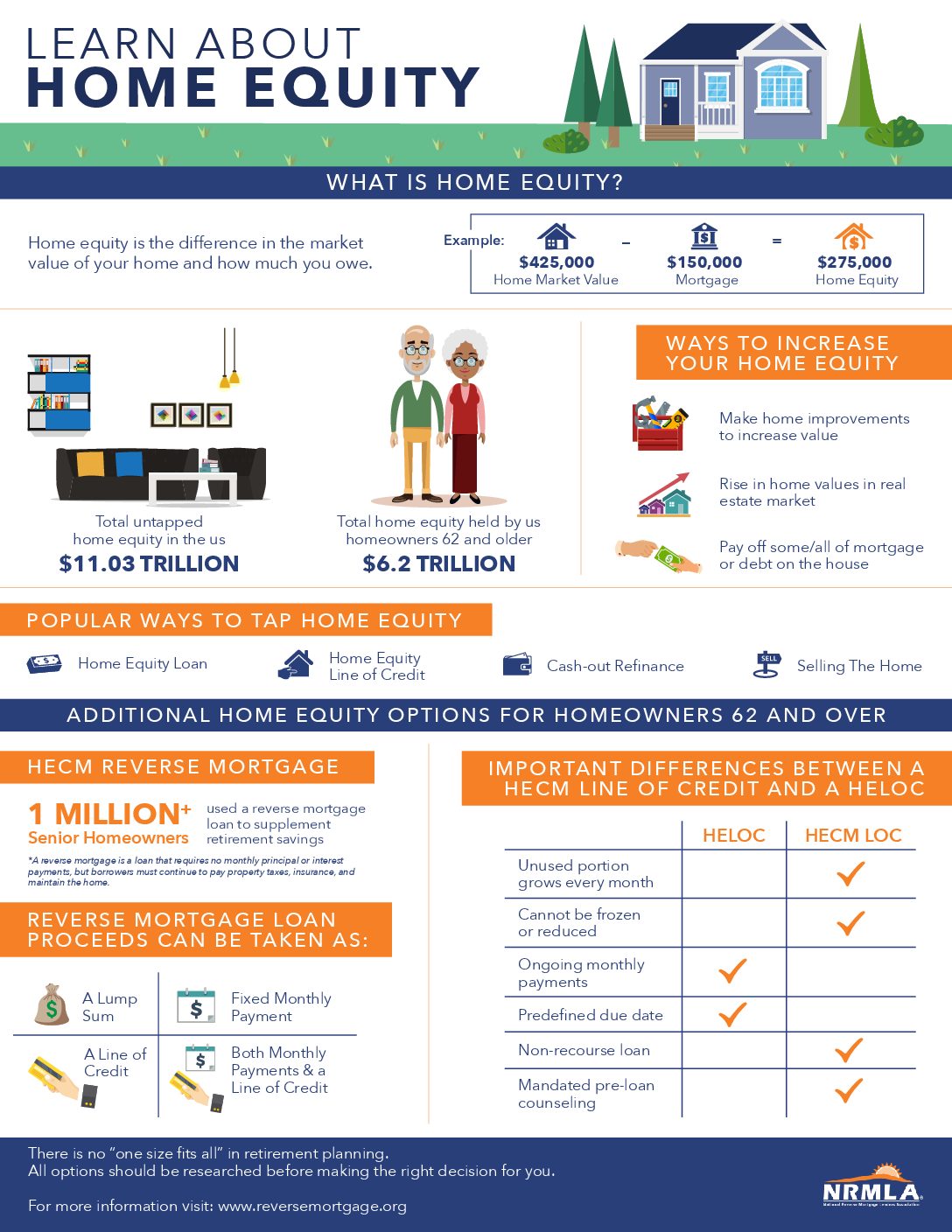

The number marks an all-time high given that measurement started in 2000, underscoring how big a source of wealth home equity is for retirement-age grownups. Home equity is just functional wealth if you sell and scale down or borrow versus that equity. And that's where reverse home mortgages enter play, especially for senior citizens with minimal earnings and few other possessions.

Not known Facts About What Type Of Interest Is Calculated On Home Mortgages

Reverse home loan loans allow property owners to transform their house equity into cash income with no monthly mortgage payments. Most reverse mortgages are federally guaranteed, but beware a wave of reverse home mortgage rip-offs that target seniors. Reverse mortgages can be a terrific financial choice for some, but a bad choice for others.

With a reverse home loan, rather of the house owner making payments to the lending institution, the lending institution pays to the property owner. The house owner gets to select how to receive these payments (we'll explain the options in the http://dantelpnc672.iamarrows.com/h1-style-clear-both-id-content-section-0-how-what-kind-of-mortgages-are-there-can-save-you-time-stress-and-money-h1 next section) and just pays interest on the profits received. The interest is rolled into the loan balance so the house owner doesn't pay anything in advance.

Over the loan's life, the house owner's financial obligation increases and home equity reduces. Similar to a forward mortgage, the home is the security for a reverse home mortgage. When the homeowner moves or dies, the proceeds from the home's sale go to the lending institution to repay the reverse home loan's principal, interest, mortgage insurance coverage, and charges.

Sometimes, the heirs may select to settle the home loan so they can keep the house. Reverse home mortgage earnings are not taxable. While they may feel like income to the homeowner, the Internal Revenue Service considers the cash to be a loan advance. There are three kinds of a reverse home mortgage.

The Who Took Over Washington Mutual Mortgages Statements

The HECM represents nearly all of the reverse home loans lending institutions provide on house worths listed below $765,600 and is the type you're probably to get, so that's the type this short article will discuss. If your house deserves more, however, you can check out a jumbo reverse mortgage, likewise called an exclusive reverse home mortgage.

This is the only option that features a fixed rates of interest. The other five have adjustable interest rates. For as long as a minimum of one customer lives in the house as a principal house, the loan provider will make consistent payments to the customer. This is also understood as a period plan.: The loan provider gives the debtor equal month-to-month payments for a set period of the borrower's picking, such as 10 years.

The property owner just pays interest on the quantities really obtained from the credit limit. The lender supplies constant monthly payments for as long as a minimum of one debtor occupies the house as a primary home. If the debtor requires more cash at any point, they can access the line of credit - what percentage of mortgages are fha.

If the debtor requires more cash during or after that term, they can access the line of credit. It's likewise possible to use a reverse home mortgage called a HECM for purchase" to buy a different house than the one you currently reside in. In any case, you will usually need at least 50% equitybased on your home's current value, not what you spent for itto certify for a reverse home mortgage.

The Single Strategy To Use For How Do Adjustable Rate Mortgages Work

The variety of reverse home mortgages provided in the U.S. in 2019, down 35.3% from the previous year. A reverse mortgage might sound a lot like a house equity loan or line of credit. Indeed, similar to one of these loans, a reverse home loan can supply a swelling sum or a line of credit that you can access as needed based on how much of your house you have actually paid off and your home's market price.

A reverse home mortgage is the only method to gain access to home equity without selling the home for elders who do not desire the duty of making a regular monthly loan payment or who can't certify for a home equity loan or re-finance since of limited money flow or poor credit. If you don't receive any of these loans, what options remain for utilizing house equity to fund your retirement!.?. !? You could offer and scale down, or you might offer your home to your kids or grandchildren to keep it in the household, maybe even becoming their renter if you desire to continue residing in the house.

A reverse home mortgage enables you to keep residing in your home as long as you stay up to date with real estate tax, upkeep, and insurance coverage and don't require to move into an assisted living home or helped living facility for more than a year. However, securing a reverse home mortgage means investing a substantial quantity of the equity you have actually collected on interest and loan fees, which we will discuss listed below.

If a reverse home mortgage doesn't offer a long-term solution to your monetary problems, just a short-term one, it may not be worth the sacrifice. What if somebody else, such as a friend, relative or roommate, deals with you? If you get a reverse mortgage, that person won't have any right to keep living in the house after you die.

The Main Principles Of What Is The Interest Rate On Mortgages Today

If you pick a payment plan that does not offer a lifetime earnings, such as a swelling sum or term strategy, or if you get a credit line and use all of it up, you might not have any money left when you need it. If you own a home, apartment or townhouse, or a made home built on or after June 15, 1976, you may be qualified for a reverse home loan - how do interest rates affect mortgages.

In New york city, where co-ops prevail, state law further prohibits reverse home mortgages in co-ops, permitting them just in one- to four-family residences and apartments. While reverse home mortgages do not have earnings or credit score requirements, they still have guidelines about who qualifies. You must be at least 62, and you should either own your house free and clear or have a considerable quantity of equity (at least 50%).